Crops > Outlook & Prices > Outlook & Prices

January 2021

Factors driving prices

Crop prices have been on a tear since the derecho in August. Nearby corn futures have risen from $3.25 per bushel then to nearly $5 per bushel in the first week of January. Nearby soybean futures have gained nearly $5 per bushel during that same time. The bulls have come out to play over the past five months. There are several factors supporting these runs. Concerns about drought continue to hang over production outlooks in both South America and the US. Labor disputes and a strike have hampered South American exports. But arguably, the two most important factors supporting US crop prices today are the pace of US export sales and speculator interest in the crop markets.

Let’s start with the export sales. Throughout the COVID pandemic, US agricultural exports have continued to move aggressively in global markets. As the 2020/21 marketing years for corn and soybeans opened up in September, we saw the opening salvo of that surge. Figures 1 and 2 display the weekly export sales data for the 2018, 2019 and 2020 crops. The sales pace for the 2020 soybean crop has been phenomenal. Advance sales of the crop before harvest totaled roughly 1.1 billion bushels. Ten weeks into the marketing year, soybean sales had already surpassed the annual totals for 2018 and 2019. While the pace of sales has slowed sizably this winter, US soybean exports are still on a trajectory to reach record levels. China has been and continues to be the major player in this market, providing roughly 90% of the sales growth. And that’s likely understated as sales to unknown destinations (which usually end up in China) are the second largest growth area. Mexico and Egypt have also substantially increased soybean purchases this year.

For corn, the advance sales weren’t quite as strong, but recent purchases have remained stronger. As the marketing year began, corn export sales had already topped 700 million bushels. Since then, we’ve added another billion bushels in sales. With next week’s data, sales will pass the 2019 total.

USDA’s projections show a record export year for corn as well. China is the top buyer for corn this year. However, unlike with soybeans, the rest of the world has ramped purchases also. Mexico is up 10% compared to last year at this time. Japan has nearly doubled its purchases at this point. In fact, all of the top six markets for US corn are showing at least double digit percentage gains.

The strength of those export sales, combined with the smaller projections for the 2020 crops during the harvest season, provided supporting stories for speculators to buy into the crop markets. Figures 3 and 4 show the total trade and speculative interest in the corn and soybean futures markets, along with the nearby futures prices for the markets. I’m using non-commercial net trading positions to measure speculative interest. To provide some historical context, I included the data from the beginning of 2019. For corn, total corn futures trading covers roughly 8 billion bushels on average. Over time, speculators have played on both sides of the market. Sometimes being short (selling futures), looking for prices to fall. Other times being long (buying futures), looking for prices to rise. Through the 1st half of 2020, speculators gradually moved into increasingly short positions. But throughout the 2nd half of the year, speculators reversed those positions and have established significant long positions in the market. This buying spree has definitely added fuel to the corn price rise.

For soybeans, total quantities traded have been increasing over time. During most of 2019, the soybean futures market covered 3-4 billion bushels. Over 2020, it’s been 4-5 billion bushels. Speculators have been more positive about the soybean market, holding long positions more often than in the corn market. But as with corn during the 2nd half of 2020, the increase in non-commercial net long positions has aligned with the dramatic rise in prices.

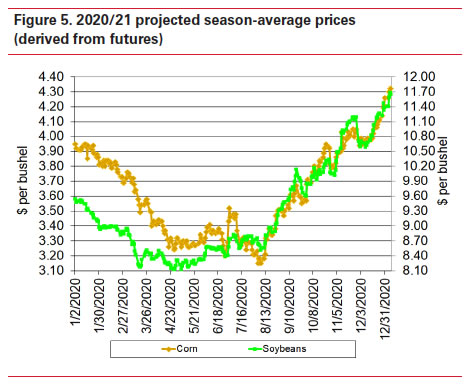

The combined firepower of export sales and speculative interest has lit a fire underneath both crops’ prices. Before the derecho, futures pointed to 2020/21 season-average prices of $3.15 per bushel for corn and $8.50 per bushel for soybeans. Now, futures indicate season-average prices of $4.30 per bushel for corn and $11.75 per bushel for soybeans. These prices have significantly exceeded USDA’s current estimates of $4 per bushel for corn and $10.55 per bushel for soybeans.

The question going forward is, can these factors continue to shove prices higher. At some point, the price increases will start to limit export desires. That may already be happening with soybeans, given the data from the last few weeks. And speculators will be quick to liquidate if they sense any weakness in the markets. For example, look back at the corn price run in May and June of 2019 and the quick turnaround in July that same year. Enjoy the run while it lasts. Luckily, for both of these factors, we get weekly updates on export sales and futures trading to monitor the situation.

Chad E. Hart, extension economist, 515-294-9911, chart@iastate.edu